The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Dicey.

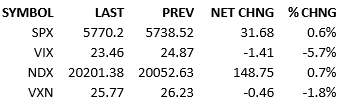

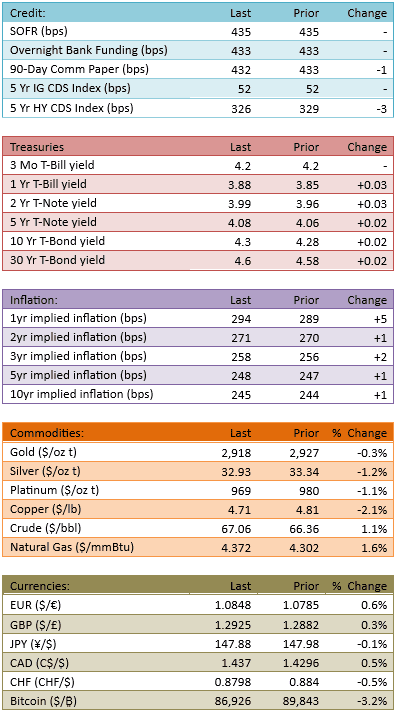

Even though the event of the day was the February nonfarm payrolls release (+151k vs +160k est & +125k prior revised from +143k), it didn’t really affect markets. S&P futures were flat just before the data and flat 15 minutes later. The index opened about -12 and rallied to +32 in the first half-hour. The index rolled over and was down 72 points on the day just before noon. The index zoomed back to flat on some confident comments from Chairman Powell and the momentum higher continued, though moderated, in the afternoon. Yields began the day lower and finished the day higher across the curve. December Fed Funds futures now price 71 bips of cutting from the Fed, that’s about 5 bips less than yesterday.

Tariff talk is jostling the market again and the market is battling around the 200-day moving average too (5733). Chart-people and fundamental people are weighing significant developments in their respective worlds, at the same time. It’s resulting in some herky-jerky moves that are getting exaggerated by the momentum players. Frankly, it’s a mess. The only positive from all this is that things haven’t gotten so unbalanced that the S&P zoomed off 2-plus percent in some direction.

Going into the weekend, the bulls get the hip tip for the session, but the bears win the week. Most investors are relieved that the tape is showing signs of life and I’m sure they will come out swinging on Monday morning, assuming innocuous news over the weekend.

The usual questions remain however. Is the US, and global, economy slowing? Is the slowing significant enough to derail risk assets? Are we on an unalterable course?

Today’s labor data, on its face, gives comfort to the longs because it looks like labor is still pretty healthy. The miss was small and the absolute level of hiring is still great from a historical perspective. The 10-year average NFP is +153k. However, DOGE layoffs on en route to the official labor data and private sector layoff announcements have been popping up in the headlines for the last two weeks. The labor data will likely get worse.

How will stocks react when those weak numbers start showing up? Will stocks be shocked or are they currently ready?

I don’t know but I get the feeling that US stocks are living in the moment and not paying close enough attention to the trouble around the corner.

See you Monday, have a great weekend.

-Mike

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.