The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Too strong labor

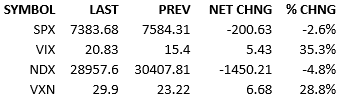

Futures were slightly lower in the premarket but markets were calm until nonfarm payrolls (+172k vs +88k est and +179k prior revised from +115k). Interest rates jumped, as did the Dollar, while the equity futures dropped. Fed-hiking predictions showed up in the Fed Funds futures market and chatter about a tighter Fed policy to fight inflation spread. With inflation pressures on everyone’s mind thanks to crude, and a tight labor market due to an accelerating economy, investors reacted in the old school way, where good news is bad news. Equity selling momentum built over the day as most stock investors used this as the perfect excuse to take risk off the table. The S&P lost almost 2.7% by the close. Capital flow was expectably heavy at 134%.

So today was a fundamental catalyst that favored the bears. The market was overbought and sentiment was euphoric. May nonfarm payrolls was the straw to break the camel’s back. The question is whether dip-buyers will pounce on Monday or if we’re in for a bearish stretch of trading.

The sentimental pendulum changed direction today. Chart-watchers will note that there’s a lot of downside remaining until the usual moving averages suggest getting longer. The 200-day MA is 7155. The 100 and 50 are 6995 and 6858 respectively. If that’s the kind of downside ahead of us, we’re going to see sentiment get pretty negative toot sweet.

Personally, I don’t think we’re going down that far. The market got a little spooked by the hypothetical of a Fed-hiking policy path. That is quite a tall order. It’s certainly not impossible but I think it’s a longshot.

If the Fed makes noises about being patient, watching the data, anticipating lower inflation with a resolution to the US/Iran conflict, markets will return to risk-taking. The Fed makes its next decision on June 17th, not very far away. It would not surprise me if Fed Governor or two make some market-calming comments Monday. We’ll see.

One last thing, while a hot jobs market has historically influenced the Fed to be biased to hiking, we have experienced a lower unemployment rate over the past 4 years without seeing wage-driven inflation. That fear, as well as the policy response, has roots in the 70s and has been debated since then. We could be in a new economic regime where both policy-makers and investors no longer see a robust labor market as a trigger of inflation.

My point is that if the labor market is strong, both the Fed and the market could make peace with that and not think that higher rates were necessary. It will eventually come down to the CPI and PPI. The next data points for those arrive Wednesday and Thursday respectively.

Have a great weekend. See you Monday.

-Mike

Visdom Market Commentary

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.