The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Intraday jitters

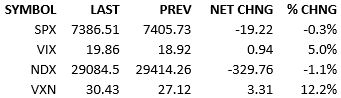

The premarket was quiet and capital markets were moving in the risk-on direction. Yields were falling and stock futures were bid. The S&P 500 opened +45 and was nicely higher until the late morning. The tape slid, led downward by tech, and there were no smoking gun headlines to blame. Most other sectors remained positive but tech, and also energy, were significantly sold. Late in the lunch period, President Trump posted that the US would need to retaliate for Iran’s downing of an Apache helicopter last night. This news prompted the usual war-is-worsening reaction in markets. Crude spiked, yields climbed, the Dollar climbed, precious metals fell, and stocks fell. After the initial shock of the President’s post, markets stabilized and calmed, retracing some of the moves which occurred with the President’s post.

So much for a quiet session. US equities are sensitive to US/Iran news today, after essentially ignoring it yesterday. Who knows where this leads us going forward but, unless peace is about to break out, stocks are going to have a tough time going north while investors are so jittery.

Maybe tomorrow’s CPI data (+4.2% est vs +3.8% prior) will help, but it will have to deliver a cool surprise to do so. If the number comes in hot, the bears are going to feast.

Setting aside the potential inflation catalyst coming tomorrow, we should step back a bit and consider where the drop in stocks since the 2nd leaves us.

This selloff is not a small dip. The market has dropped significantly. The chart is not broken but the conversations can be started about whether we are at risk of breaking soon. The index remains above the 3 major moving averages, so technically, most chart-followers should continue to lean bullishly. The bullish trend, in medium to longer time windows, remains intact.

How much conviction do the dip-buyers have still? The chart is not broken but it looks fragile and vulnerable. Is that risk obvious enough to back-off the usual buyers? We have experienced a tremendous extension of the existing bull market since April. A pause and/or a pullback was to be expected. It has arrived and it is here, but it’s been a bit faster and sharper than most bargained for.

I think today’s intraday jitters show us that the market is not ready to bounce fast and resume its run to the stars. Even if inflation data provides an assist to the longs tomorrow, I think time is needed before a significant new upside leg can breakout.

See you tomorrow.

-Mike

Visdom Market Commentary

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.