The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Repricing?

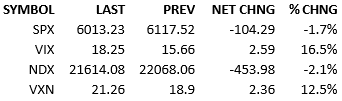

Everything was normal until regular trading began. The S&P 500 opened down 5 and leaked value slowly until 9:45AM. Various Global PMIs printed which showed a contraction in the services segment of economic activity. The S&P dropped a bit more at 10 AM when U Michigan data showed less enthusiasm for economic conditions and outlooks. The S&P legged down again at midday and stories of a new coronavirus in Wuhan spooked investors further. By 2 PM, it was obvious that there would be no intraday bounce and traders abandoned trying to bargain hunt. Flow was heavy at 125% and yields came in materially, 4-8 bips. The Fed Funds futures market now prices in 48 bips of cuts by year-end.

Price action often inspires the narrative. When futures were trading up small before the open, nobody cared about soft economic possibilities and nobody cared about the risk of viruses. Only once the market dropped significantly, did investors look at explanatory stories. The disappointing PMI data was certainly negative but the index only dropped to -17 after that information printed. After the U Michigan survey data, the index was -23. The coronavirus story comes from a paper published two days ago, but it caught investor attention today. Once the S&P was off more than 50 points, the narrative emerged that markets are worrying about slowing economic activity and the risks of external shocks.

My point is that the weakness in the market appears to have inspired the search for, and attachment to, some fundamental narratives and not the other way around. That said, the market’s multiples are priced for good news only. With a sprinkling of bad news today, some may be reconsidering their fair values for the market. And once downside momentum gathers steam, there’s a lot of momentum players who hop on the short side too.

I am not worried about today’s developments causing a calamity. I do think that today is a symptom of our excessive valuations. We cannot be robust to negatives at stretched valuations. Maybe this is a repricing. I doubt it but it’s possible. If that’s true, this is the start of a process. The process accelerates with negative news. Maybe the process is prolonged with good news and good old-fashioned denial. We’re just going to have to wait and see.

I don’t want to be a bear. I don’t see the upside scenarios outweighing the downside ones. I think the risk/reward is bad for the longs. The bears need a negative catalyst to pay them off. Maybe some of those stories are around the corner. Maybe Nvidia’s guidance on Wednesday will disappoint. I can see the case for the shorts. I just wonder how willing they are to act. They’ve been skinned alive for years.

See you Monday, have a great weekend.

-Mike

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.