The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Tariffs.

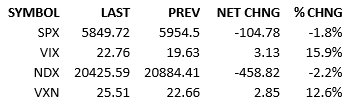

Overseas markets climbed nicely today, climbing in response to the big rally we experienced Friday. Futures were up about 25 points in the premarket. Premarket economic data was uninteresting. The index opened +15 and climbed for 2 more minutes. The index rolled over quickly and went negative 20 minutes into the session. 10 AM economic data showed slower growth than expected and higher inflation. The S&P plunked down 20 points on that data. The index came back quickly and made it to unch’d a few times before lunch but the sentiment damage was notable. Bulls and dip-buyers were making a go of things but the tape was heavy and it gave way in the afternoon. The index was off 55 points when President Trump made comments that 25% tariffs were definitely coming for Mexican and Canadian trade. The index dropped 50 more points in short order. Yields went from higher this morning to lower this afternoon. Fed Funds futures now price 71 bips of cuts for 2025. That’s almost 3 cuts now. It was a little more than one in mid-February.

Sentiment is now in the process of changing. It kinda sorta changed last week and the week before but the market didn’t wholeheartedly believe that economic growth was at-risk. The market kinda sorta though that we were experiencing the same old, same old opportunity to buy the dip and rip back to new highs. The risk-off and risk-on behavior was kind of like a sputter. Perhaps that was due to market participants being stubborn to the new data and behaving according to the playbook of 2023 and 2024.

Regardless of what explains the recent price action, now the market is starting to think about a slowing economy. The market is starting to think about what actually implemented tariffs mean. These are bearish transitions. We are also coming to these realizations from a place of very high valuations. This means the downside could be scary.

Who knows what the coming economic data will do to the market in the short-term? It will likely be negative however. If the growth is slowing, or contracting, the market isn’t prepared to confront that reality. It’s going to come as a nasty surprise to many.

I still don’t believe we’re on the verge of a bear market. I do think the valuation correction is going to make it feel that way though.

Don’t have an itchy trigger finger with your buy buttons. The sentiment pendulum has not swung out of optimism yet. It will overshoot to the negative but we’re not there yet.

See you tomorrow.

-Mike

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.