The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Bounce.

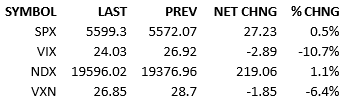

Like so many past days, S&P 500 futures traded higher overnight. Futures added to their gains as Europe traded and by 8 AM they implied 40 points of upside for the index. Feb CPI YoY (2.8% vs 2.9% est & 3.0% prior) data helped the bulls in the moment. The index opened trading around +60. Morning bears showed up as usual and drove the index into negative territory around 11 AM but the dip only lasted 30 minutes. Buyers ramped prices higher as fast as they sunk and the S&P traded around +40 points for the bulk of the day. Tariff talk continues to concern markets but it didn’t bother US stocks very much today. Growth concerns lessened a touch today as well with Fed Funds pricing 69 bips of cuts in 2025.

Longs certainly welcomed today’s gains. The headlines, which were blah, didn’t have much to do with the rally however and while the softer CPI data was helpful, it wasn’t critical. The market seems to have digested the slower growth trajectory of GDP and is factoring in a probability of recession going forward, albeit a small one. Perhaps this means that we’re in a trading range appropriate for the current perception of the investment landscape. I think this is a reasonable conclusion. Upside and downside from here won’t be very interesting, until we get some new material news.

What do we think the next major surprise will be? That answer should dictate our equity posture for the here and now.

Major economic releases are *not* likely to be a catalyst for a while. The data is mostly from February and slow to react to economic shifts anyway. Weekly jobless data (225k est vs 221k prior) is a different animal though and it releases tomorrow. It’s from last week but it could show the first DOGE effects. If the number surprises strongly, I think the market will ignore it. Investors will just tell themselves that the DOGE data is delayed. If it shows significant weakness, the market will react badly. It’s a bad setup for the bulls, I think. We shall see.

Setting aside the weekly jobless data, what other news development might materially surprise the market? Tariff talk is high on the list. Currently the rhetoric is bad and heading towards worse. Almost every headline covers a new tariff in retaliation for a prior one. The market is starting to get accustomed to only bad news on that front. What if Trump and some major trading partner come to a quick and clean agreement? That kind of good news would certainly spur bulls onward and upward. That might be a true tradeable bottom

The question for us is… how likely is a bolt-from-the-blue trade agreement?

By definition, it could happen at any time. I think everyone is going to have to feel some significant pain before leaders come to the table to fix things.

Have you felt significantly pain? Has the public? Have the overseas trading partners?

Not yet.

For that reason, I think more pain is coming until tariff news will be ripe to surprise to the upside.

See you tomorrow.

-Mike

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.