The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Downside resumes.

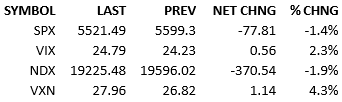

Yesterday was a brief respite from the equity market declines and today the selling continued. News was a snooze although tariff talk has heated up again. Today the headline is 200% tariffs on European wine if the EU slaps a tax on US whiskey, which is an EU retaliation for US tariffs on EU steel and aluminum. It’s a mess that is getting messier. Anyway, that story simply illustrates the reason for the shifting mood in the market. Things are getting worse and worse and so goes investor sentiment. Cooler PPI YoY (3.2% vs 3.3% est & 3.7% prior revised from 3.5%) this morning didn’t help the longs and stronger than expected weekly jobless data (220k vs 225k est & 222k prior revised from 221k) was ignored. The index opened trading -10 and leaked significant value after 10:30 AM. The index spent the rest of the session down more than a percent. Treasury yields flipped from up to down over the day and Fed Funds are pricing 74 bips of cuts for the year today.

Growth concerns continue to weigh on the market. While there were no smoking gun news stories to point to this, the Treasury yield intraday flip, the jump in Fed Funds cutting expectations, and the sector performances for the day suggest we’re on to something. Utilities performed best and gained while communication services and consumer discretionary performed worst.

We are in the midst of a mood/sentiment adjustment. The selling will stop when the moods swing back toward optimism. We are not there yet.

So we ask the question, when’s the mood going to improve?

Yesterday I made the case that *positive* tariff news would be a good catalyst. I also made the case that *positive* tariff news is off in the future, on the other side of significant pain for everyone.

If we have to wait for positive tariff news, we’ll be waiting for quarters. It’s going to be a bad stretch.

I’m not sure what other news might turn market attitudes. Perhaps something unexpected that forces everyone to toss away recession expectations. What could that be? I’m not sure but whatever it might be would be close to a miracle.

We’re in a situation where fundamentals are *not* going to turn sentiment. Sentiment will have to turn first, by itself.

That sends us into the realm of chart-watching. We need to pick a price point way below here, where even the pessimists say that the prices are worth the risk.

Let’s look at everyone’s favorite chart.

Your guess is as good as mine. Maybe 5200 looks like a decent buying point? 5000 looks like the best possible price on the chart. Of course, if things get really ugly, we could break below all the supports on this chart and trigger an official bear market.

Hold on to your hat and your lunch. If fear shows up, stocks are going to get mugged.

See you tomorrow.

-Mike

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.