The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Pam Ewing.

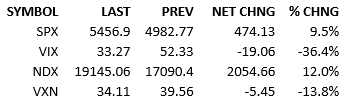

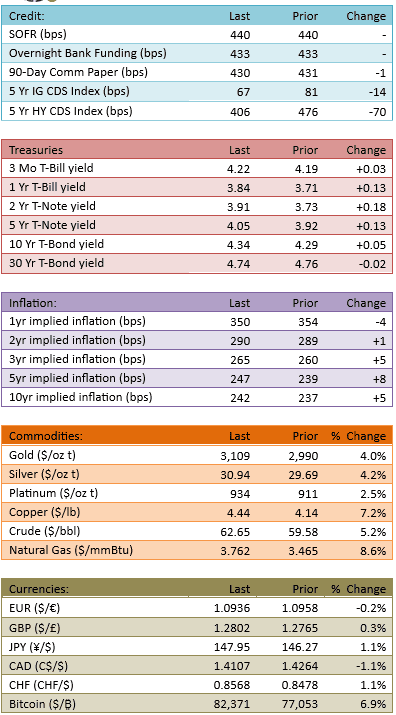

It was all a bad dream. Markets rocketed up on the news from President Trump that the tariffs would be paused for 90 days, except for China. All the computers bought, all the shorts bought, all the nimble actors bought. It was a bonkers upside rally. Capital flow was incredibly heavy at 212%. Yields climbed enormously across the curve. Priced Fed cuts are now 79 bips for the year, a 23 bip change from yesterday!

We are not going over the economic cliff. Will we go over it in 90 days? Who knows? The market doesn’t worry about that right now. The market is attempting to erase all the damage since Liberation Day. Is that warranted?

The argument for yes is being embraced by stocks right now. The view is that the tariffs won’t ever really go into effect, except for China, and given the health of the US economy, we should be able to sustain positive but lower GDP growth.

The argument for no is that the red light/green light game of economic policy by the President has materially cooled economic animal spirits. US GDP will slow and the slowing will force US equity revaluation. A recession is still quite likely, which the market has essentially taken off the table today.

We haven’t had a 1-day S&P rally like today since March of 2020, during the COVID volatility and also October of 2008, during the Global Financial Crisis volatility.

The longs are partying, and with good reason. Understand a few things before you put a lampshade on your head.

Are valuations proper for the no-tariffs-except-on-China future?

Are valuations proper for the recession-is-coming future?

I think the answer for both questions is no. I wonder what the market will conclude once the mother of all short squeezes finishes.

See you tomorrow.

-Mike

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.