The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Bad to worse.

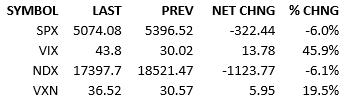

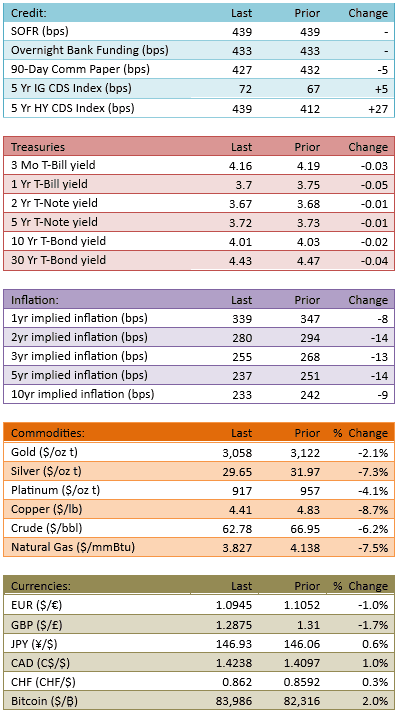

Overnight was bad, early morning was worse, regular trading hours were worst. Tariffs and a trade war are what we’re dealing with. How much economic suffering will result? That’s the one and only question. There’s no need to delve into the nitty gritty details of the day. Let’s go right to the big picture.

It is time to take inventory of the state of the world and what the markets are telling us.

Let’s look at the US economy.

There’s more but I think you get the point.

Recession is the worry. Most economists are only bumping up their probabilities of a recession this year. The Atlanta Fed is telling us it’s already here yet most economists only moved their probabilities from 10-ish percent to 30-ish percent. I don’t know what they’re collectively smoking. Polymarket recession probability jumped to 56% today, up from 39% on Mar 31.

If economists are in the 30-ish percent camp and the online market is 50-ish percent, you know the global financial markets aren’t far away from that range.

So here’s the key takeaway, *if* a recession is coming, the markets *still* aren’t priced for it. Pain will continue.

I wish I had better things to say. The market is still in partial denial about what’s happening. I think markets still think that Trump will get concessions from all the other countries in a mere matter of days and all the tariffs will go away like a bad dream.

One can never say never but that is a wing-and-a-prayer kind of theory. I certainly don’t think you bet your portfolio on that scenario.

The world changed Wednesday after the close. People and markets are still adjusting to that change… and significant pockets of investors are in denial. That’s not a recipe for a bounce.

Last point.

It doesn’t matter if the tariff gambit is a wise strategic move or a stupid blunder. Strip the value judgements out of your thought process. In the moment, in the here and now, this is a recessionary action that is smothering economic activity. This is what bear markets are made of.

A new bull will only show up once the market starts to perceive economic activity is on the upswing. That ain’t happening anytime soon.

See you Monday, have a great weekend.

-Mike

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.