The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Rumor mill.

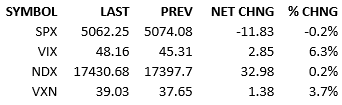

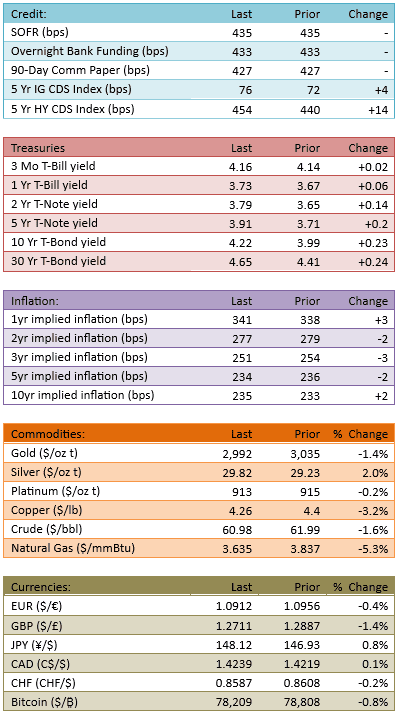

Overseas markets were clobbered. S&P futures were off 3% overnight. The market opened and the S&P rapidly lost more value, the morning low was 15 minutes into trading and the index was down 4.7% for the day, well below the official bear market level of 4915. At that point, the market bounced very strongly and then a tweet sped through the market like a bat out of hell. The tweet stated that Trump was considering a 90-day pause in tariffs for all countries except China. The S&P went up 400-plus points, more than 8% in less than 30 minutes. The tweet was refuted by the White House and called fake news. The market fell back incredibly quickly and somewhat below Friday’s close. We wandered through the remainder of the day about that level. Capital flow was extremely high today, 228%. Yields climbed significantly across the curve.

The range of trading today, thanks to the rumor mill, was the largest percentage since March 13, 2020. That was a session early in the pandemic. Considering that the pandemic was one of the fastest shocks to markets and economies, as well as a period of extremely high uncertainty, should put the last half week into perspective. Whether you agree or not, the market is as worried and as in-the-dark as it was when the pandemic just began. Let that sink in for a moment.

Having seen an 8% intraday bounce, on tariff talk, even though it was fake, should remind us that these are not normal markets. With the specter of tariffs hanging over the markets, investors and robots are on hair-triggers. Right now, the stampede *into* stocks is the outlier possibility. There remains significant chance that equities continue to drop, but this seems to be a process of consistent downward pressure. As markets come to accept tariffs as longer-lived realities, the market drifts lower with the capitulation of various investor groups.

I don’t want to argue that a crash is unlikely but I do want to suggest that the market may be structurally reversed for the foreseeable future. Stocks may now be on an escalator down and an elevator up.

Tariffs are all that matters. You know it. I know it. We’re all just watching the White House for policy shifts and the economic data for the consequences. That said, guess what starts tomorrow?

Earnings season.

Walgreens Boots Alliance kicks off the S&P 500 companies tomorrow morning but it’s doubtful that will matter to the market. JP Morgan and a few other banks announce Friday morning. The results will be lightly regarded. The guidance will be the only thing that investors will want to digest. We can only wait.

In the meantime, hold on to your hat. Tariff talk is the market and the market is tariff talk.

See you tomorrow.

-Mike

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.