The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Nvida and Powell.

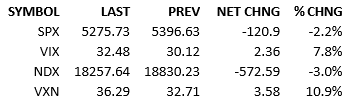

Nvidia announced a $5.5 billion charge last night due to an export ban to China. The stock fell 5% overnight. That sent a risk-off impulse through markets and S&P futures were off around 30 points come today’s early hours. The index tried to recover before lunch but rolled over and stabilized in the down 70 point range when Chairman Powell spoke and markets soured from there. He didn’t say anything specifically to shatter investor sentiment but what he said splashed cold water on the longs. If investors were kinda sorta hoping for the Fed-to-the-rescue-ASAP, his comments yanked that dream away. Downside momentum took over and the day took an ugly turn in the afternoon. Capital flow was surprisingly light considering the stock market’s move, 91%.

Today was a sentimental hit. At best, it is a short-term blow to the optimists. Dip-buyers certainly hope that’s the case. Powell didn’t tell us anything we didn’t already know. We’ve *always* known that the Fed doesn’t swoop in to help the shareholders. They swoop in to rescue the economy and/or the financial system. So the market should have known that the Fed wasn’t about to drop rates to keep stocks elevated. So this isn’t *new* news. That’s the spin by the dip-buyers. They have a point too but…..

Sentiment may have truly shifted for a prolonged period as a result of this Fed communication. With the Fed waiting to *see* the damage of the tariff talk and also waiting to *see* how inflation changes due to the mix of economic slowing and tariffs… that means the Fed will act *after-the-fact.* That’s off in the distant future as far as markets are concerned. So the market is *on its own* until the economic damage is in place and the Fed is compelled to respond. Instead of hoping the Fed would pilot the market through treacherous waters, it is going to come in to help/rescue the market *if* we’ve already crashed onto the rocks. That means pain is almost certainly coming. It means that avoiding a valuation compression is highly unlikely.

So here we go. Prices came down quickly this afternoon and I don’t see a strong reason for them to go up anytime soon. The recession-won’t-happen camp just lost a bulwark. What’s left for them to count on? The answer is simple, an unexpected robustness in the economy. That’s not a delusional possibility but it’s a longshot.

The bottom line of today is that we got rocked by a sentiment one-two punch. The Nvidia news took money and hype out of that high-flyer’s sails. It was small dose of reality. The Chairman Powell interview was a bigger blow to equity optimism. The Fed was a key ally that was counted on to keep recession at bay. That idea is out the window and investors are re-framing their views accordingly.

The reason why I think sentiment has truly shifted versus taken a brief bearish turn is that both the Nvidia news and the Powell news are fundamental, unlikely to change, and set the stage for a few months. Economic activity is changing and investors have been reluctant to extrapolate the negatives beyond marginally. The reasons have been various. Those reasons are running out.

Last thing. Tomorrow is the last trading day of the week. Markets are closed Friday. Weekly jobless (225k est vs 223k prior) will be a closely watched number and with investors sensitized to negatives, a bad print could really cause pain.

See you tomorrow.

-Mike

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

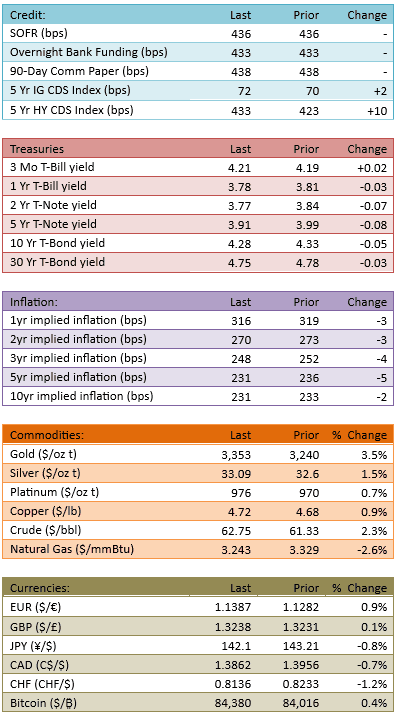

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.