The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Auctions?

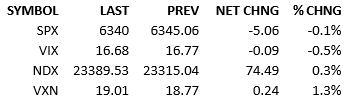

Things looked pretty typical early on. S&P 500 futures rallied a little overnight and significantly further during European trading. The index opened +35 and wandered up there until 10 AM. June Final wholesale inventories (0.1% vs 0.2% est & 0.2% prior) disappointed at that time but this was not the cause of today’s selling, it just coincided with the beginning of the slide. The tape traded heavy for the rest of the session. The trend was consistently down, slow, and calm. Bulls made efforts to turn the tape but they didn’t work until late. In the afternoon, a weak 30-year Treasury auction threw cold water on investor appetites for equity upside. Yesterday had a weak 10-year auction too, which was ignored. Now people are perking up their ears and wondering is something is amiss. Interestingly, the yield curve didn’t move much today. So whatever we *suspect* might be negative about these recent auctions, it’s not bothering the Treasury market.

Maybe we’re just playing some chart-games right now? We had dips, we had subsequent rallies, leading to subsequent dips. There are no major technical levels in play so whoever is trading technically, they aren’t all using the same consensus signals. It might explain the alternating blows between the bulls and bears.

Tariff talk was in full effect again today. The tasty morsel of the moment concerned microchips. There will be huge tariffs on chips unless they are built in the US. Of course, there isn’t much chip manufacturing here so the tariffs will be devastating although they can (will?) be removed if companies begin building manufacturing capability in the US immediately. Apple announced a $100 billion investment from the Oval Office so they will be exempted from the tariffs (we think). AAPL stock rallied nicely today in response. It *appears* that Apple has been working with the President to accommodate his wishes and avoid the nasty tariff consequences that pressured the stock for most of the year.

Tim Cook gets the attaboy of the day.

Anyway, like so much tariff talk, we only think we know what we need to know and we can only wait and see for how the President changes things at some point down the line. It’s quite a predicament.

The macro calendar is uneventful tomorrow so if a catalyst is going to shake up the markets, it’ll probably come from the White House. I wonder what’s in store.

If the White House is actually quiet, we’re looking at a summer Friday with the S&P up more than 1% for the week, about 2% below the all-time highs, and about 2% above the August lows.

That’s not technically compelling for a bull nor a bear. I guess the tiebreaker goes to the long-term trend… I’ll give you three guesses about who that favors.

See you tomorrow.

-Mike

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.