The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

The beat goes on.

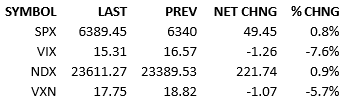

Overnight was slightly bullish, for the US at least. Overseas markets were mixed but US futures climbed. The S&P 500 opened +20 and made further gains in the first hour, climbing a bit more over the remainder of the day. Headlines were a plenty but they didn’t catalyze investors into action in and of themselves. Maybe you could argue that a *lack* of zinger announcements from the White House triggered a relief rally? Probably not but you never know. Yields didn’t misbehave while stocks rallied, climbing 2-4 bips across the curve. Climbing rates might be problematic if the bond market thought that the future was about to become unhinged but that wasn’t the case today.

Stocks, it seems, without a major news catalyst, and without strong influence from the bond market, just continued the trend. The chart looks like it’s climbing (still) so go with the flow. I think it just might be that simple.

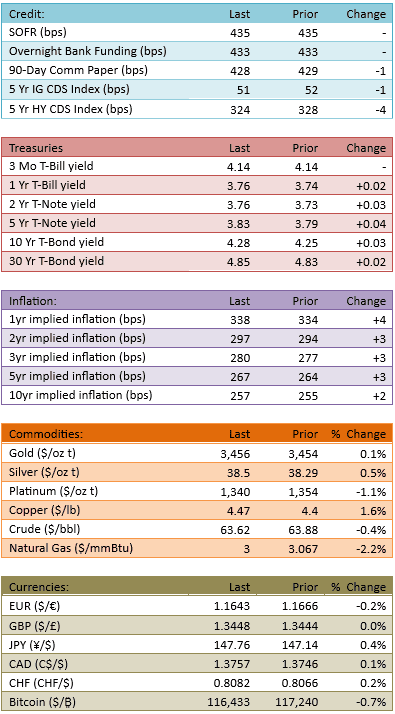

Anyway, let’s talk about rates and bonds for a bit.

Since Trump has loudly advocated for lower rates and began attacking the Fed Chairman, a long-dormant but never dead worry returned to the bond market. That’s the fear of untethered inflation set off by politically influenced monetary policy. At present, the fear remains hypothetical but possible. It keeps the bond vigilantes at their posts, the bond bears salivating, and the bond holders a bit uneasy.

At the same time, US deficits are massive and likely to grow. This requires much more Treasury supply as far as anyone can see, which also suggests higher rates out in the future.

The entire year has also been an exercise in worrying about a US economic slowdown. Everyone’s been thinking that a slowdown, or an actual recession, was coming. Rate expectations have mostly projected lower as a result. That scenario was kind of dismissed by late Spring, only to re-enter the picture with the very weak nonfarm payrolls data last week. A recession, or worse, would drop rates by multiple percent.

I realize the above is a lot to take in but here’s the summary:

The bond market is straddling two hugely different outcomes that are not too far off in the future. Much higher rates or much lower rates. It’s a battle of extremes. Bond market narratives don’t have many versions of “rates are going to hover around here.”

But that’s what’s essentially happened for the year and that *may* surprise everyone by continuing. I think today is just another step in that journey. In the bond prediction world, it’s either yield-blowout-bond-Armageddon or recession-triggered-bond-Shangri-La. When actual events split the difference, it allows the stock market to do whatever it wants to do.

Bonds and rates always matter to stocks but in this case, they will only significantly matter if they trend. If rates are all zooming higher, then stocks are going to care and bears are going to eat. If rates are all zooming lower, than stocks are going to care and bears are going to eat.

If rates keep jiggling around, going nowhere fast, stocks *aren’t* going to care and bulls are going to eat.

See you Monday, have a great weekend.

-Mike

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.