The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Cooler

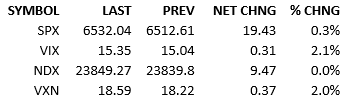

PPI (2.6% vs 3.3% est & 3.1% prior revised from 3.3%) was much cooler than expected. S&P futures shot higher and bond yields came down. FOMC probabilities moved a little. The S&P 500 opened around +27 points, tacked on about 15 more, printing fresh all-time highs. Prices rolled over around 10:30 AM. The tape drifted lower over the day, giving up the big gains of the morning. Capital flow was higher, about 120%.

The knee-jerk reaction of the morning was that inflation was coming down and so the Fed would have no reason to wait and see anymore. Fed Funds futures markets didn’t change much but equity investors breathed a sigh of relief. Equities assumed that 25-50 bips was in the bag for next week and that October would also deliver a rate cut. The reaction was that the Fed could not deliver a curve ball in the form of holding rates steady.

The equity market did not infer any sort of worry about the economy and recession risk did not become the topic du jour.

Like so many surprising data points and subsequent market reactions, we look to the next data point for more clarity.

CPI (2.9% est vs 2.7% prior) tomorrow will be scrutinized through the lens of the PPI data. Talk across the Street worries about whether producers are absorbing tariffs and other inflationary pressures or passing them along. CPI, if it looks qualitatively different than PPI, could stir up all kinds of contradictory investment theses.

I don’t know what to expect. I think a cooler number favors the bulls but I wonder if there is even such a thing as too cool? Perhaps equity investors have no concern about recession risk and they just want rates to come down faster and sooner?

Let’s find out.

See you tomorrow.

-Mike

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

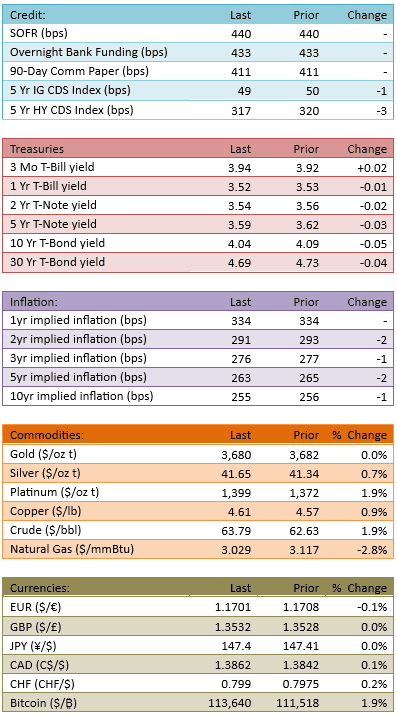

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.